World’s largest milk producer by volume, India’s dairy industry is heading into the most critical stretch of the monsoon season under a cloud of uncertainty, after the country recorded one of its driest Junes in over a century and forecasters confirmed that El Niño conditions are strengthening rather than fading. With fodder availability, grazing land, and cattle heat stress all directly tied to monsoon performance, the coming weeks of July and August will be pivotal for milk producers nationwide.

The Data So Far

| Metric | Figure |

|---|---|

| June 2026 national rainfall | 99.5 mm (approx. 40% below normal) |

| June 2026 rank since 1901 records began | 5th driest on record |

| East & Northeast India June rainfall | 197.5 mm — lowest ever recorded for June since 1901 |

| Central India June rainfall | 84.4 mm — 7th driest June on record |

| Monsoon onset delay | Approximately 10 days behind schedule in central/northwest India |

| July 2026 rainfall forecast (IMD) | Below 94% of the Long Period Average |

| July Long Period Average (LPA), 1971–2020 baseline | 280.4 mm |

| Full-season 2026 monsoon forecast (IMD) | Approximately 90–92% of LPA (below-normal category) |

| Probability of a deficient monsoon (IMD) | 60% |

| Indian Ocean Dipole (IOD) status | Neutral; possible positive shift in Aug–Sept, unconfirmed |

| El Niño outlook | Developing, expected to intensify and persist into early 2027 |

Why June’s Numbers Matter So Much

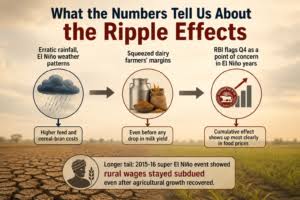

The India Meteorological Department (IMD) confirmed that June 2026 rainfall came in around 40% below normal, making it the fifth-driest June nationally since records began in 1901. The regional breakdown was more severe in places that matter most for livestock and fodder production: East and Northeast India recorded their lowest-ever June rainfall on record, while Central India — a significant belt for both dairy cattle populations and fodder-crop cultivation — logged its seventh-driest June on record.

IMD Director General Mrutyunjay Mohapatra attributed the shortfall to a combination of factors: an absence of low-pressure systems during the month, an unfavourable phase of the Madden-Julian Oscillation, above-normal typhoon activity over the western Pacific suppressing low-pressure formation over the Indian Ocean, and evolving El Niño conditions that a neutral Indian Ocean Dipole was not strong enough to offset.

El Niño Is Strengthening, Not Receding

Contrary to hopes of a fading El Niño, Mohapatra was explicit that El Niño activity is likely to continue into early 2027 and will intensify over time. This aligns with broader international assessments: the World Meteorological Organization’s April 2026 outlook flagged an increasing likelihood of a strong El Niño event developing between May and July 2026, with some models suggesting it could peak in 2027 before eventually receding. NOAA’s own update placed the probability of El Niño development at around 61% for the May–July window, with roughly a 25% chance of it becoming a very strong event.

For India, El Niño years are historically associated with weaker monsoons, higher-than-normal temperatures, and elevated pressure on both crop output and livestock productivity.

{kind=link}

Direct Line to Dairy: Fodder and Heat Stress

A below-normal monsoon affects India’s dairy sector through two distinct channels:

1. Fodder and grazing shortages. Reduced and delayed rainfall constrains the sowing of kharif fodder crops such as maize, jowar, and bajra, while also shrinking natural grazing land availability. Lower fodder output typically pushes up feed costs for dairy farmers, squeezing margins at the farm-gate level well before any impact reaches processors.

2. Heat stress on dairy cattle. Above-normal maximum and minimum temperatures — which the IMD has forecast across most of the country through July — directly suppress milk yield. Once the temperature-humidity index rises above approximately 68, dairy cattle divert energy toward cooling rather than milk production, meaning both feed intake and milk output decline simultaneously. This effect compounds fodder scarcity rather than operating independently of it.

How Markets Are Already Positioning

Financial analysts tracking rural-consumption-linked sectors have already flagged dairy as an area of potential margin pressure rather than tailwind this season. Sector commentary specifically named dairy and dairy-adjacent companies — including ice cream, dairy drinks, and beverage makers such as Dodla Dairy and Heritage Foods — among the businesses most exposed to a weak-monsoon, high-heat scenario, given their direct reliance on milk procurement costs and rural farm incomes.

More broadly, a weak monsoon tends to show up first in rural income-sensitive spending: if kharif output is affected, farm cash flows can weaken, which in turn can soften rural demand across FMCG, dairy, and agri-input categories simultaneously — a double-edged pressure on dairy companies that sell into the same rural markets they procure milk from.

One Wildcard: A Possible Late-Season IOD Shift

The clearest note of caution in IMD’s own assessment is around the Indian Ocean Dipole (IOD), currently neutral. Mohapatra noted that most models suggest a positive IOD developing in the second half of the monsoon season could partially counter El Niño’s negative impact — but stressed it is “too soon to confirm” whether this will happen, and that any such compensation would likely arrive only toward the end of August and into September. For the dairy sector, that timing matters: it would come too late to help early kharif fodder sowing, but could still support pasture recovery and late-season milk output if it materializes.

What to Watch Next

-

IMD’s weekly and monthly rainfall updates through July and August, particularly for Central India and the Indo-Gangetic plains, where fodder-crop belts and dairy cattle populations are most concentrated.

-

Reservoir and groundwater levels, which affect irrigation availability for fodder crops independent of direct rainfall.

-

IOD tracking data for any confirmed shift toward positive territory in August–September.

-

Milk procurement price trends at major cooperatives and private dairies, an early indicator of how feed-cost pressure is flowing through to farm-gate economics.